So you are buying a brand new car, or a used vehicle from a dealership! Congrats on the new vehicle! If a bank is involved in some way shape or form for financing this vehicle whether it is an auto loan, or a leased vehicle – the insurance requirements can be specific. But luckily I am here to explain it to you.

Lets say you get an auto loan to finance a brand new car. A bank is going to require you to carry two coverages. These are “comprehensive coverage” and “collision coverage”, also often just referred to as comp and collision. Some people may also refer to it as “full coverage”, but this term of full coverage may be a little misleading. Many people may mean different things when they say full coverage, for example some people may consider towing coverage included in their definition of full coverage. The bank does not require you to have towing, rental car, or even full glass coverage when financing a car. Typically, a bank is going to require you to have comprehensive and collision coverage at a deductible of $1000 or lower. Some banks make it a $500 deductible or lower, but by far in my experience the majority of banks require it to be $1000 or lower. Check specifically with any bank you finance an auto loan with. Along with that, they will be required to be listed as an additional interest and loss payee. This just means that if you total your car, payment will be issued to the bank in order to protect the loan they issued you.

Banks will want you to have comprehensive and collision coverage on your vehicle to protect their investment. If you total your car and don’t get it repaired, and lets say you also don’t pay your auto loan, then they would have nothing to repossess in the event of you not paying the loan off. So this forced coverage by the bank protects their investment.

Leasing a car can have additional requirements. While it will typically also include the same deductible requirements usually at $1000 or lower, it will also require certain levels of liability. A majority of leasing companies will require $100,000 per person, $300,000 per accident, $50,000 property damage liability coverage. Some leasing companies do not require this, and always check with your financing company, but a vast majority do require this. The reason for that is that the leasing company is listed on the title of the car since you do not own it, meaning they open themselves up to a certain amount of liability.

Overall this should help inform you on the correct kinds of coverage you are going to need when leasing or financing a vehicle in New York.

When registering a vehicle in your name, the DMV is going to require a couple of things from you regarding insurance. The New York DMV can be very particular about their insurance requirements. This page is dedicated to the insurance requirements only, for more information about DMV fees, registrant requirements, and other information please see this link.

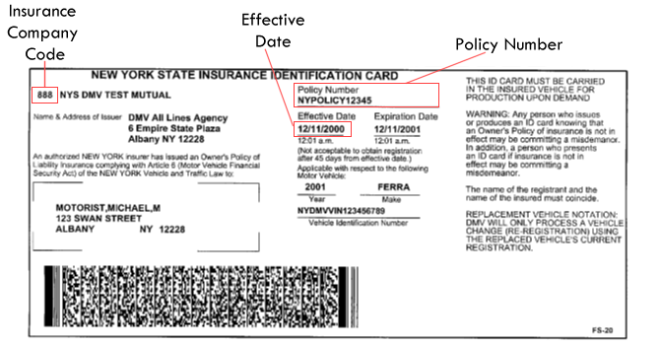

So you want to register a car in New York, what kind of insurance are you going to need? The DMV only requires one thing, an ID card with your name on it with the VIN number of the car you are insuring. An ID card shows the DMV that you have New York Compliant liability insurance. The state minimums for liability insurance are $25,000 per person, $50,000 per accident, and $10,000 for property damage. If you insure a vehicle with these liability limits or limits that are higher, then the insurance company you work with will provide you an ID card.

An ID card has a couple of key qualities. It will have your name, a bar code, your address, the VIN number of the vehicle, the effective date of the policy, the policy number, The year and make of the vehicle, and the company name, address, and company code.

In order for the insurance ID card to be valid, in New York State the ID card must match your license. The New York DMV is extremely particular about how the ID card appears. This may sound silly or irrelevant, but in order for the DMV to accept your insurance ID card it must be formatted a certain way. If you have a middle name on your license, the insurance ID card must have your full middle name or a middle initial or else the DMV will not accept the ID card for registration. The insurance ID card has a character limit, meaning names may be formatted in a way different to how it appears on your license.

Here are some examples of how an ID card may appear depending on what appears on your license.

Example name: John Smith

If your name is John Smith, the name on the ID card will appear as

Smith, John

Example name: John, C, Smith

If your name appears on your license as John Smith with a middle initial of C, the name on the ID card will appear as

Smith, John, C

Example name: John, Charles, Smith

If you name appears on your license with John Smith and a middle name of Charles, the name on the ID card can appear as either:

Smith, John, C OR Smith, John, Charles

At the time of posting this, you do not need the full middle name in order for the insurance ID card to be valid, but with new regulations regarding the REAL ID it is possible it will change to HAVE to include the full middle name.

Example name: Johnathan, Xavier, Smithersonian

If your name appears on your license as Johnathan Xavier Smithersonian, this name may be too long to fit on an ID card. Because of this, the name on the ID card must truncate to something shorter. So it will appear as:

Smithersonian, J, X

Example name: Johnathan Charles, Xavier, Smithersonian

If you have two first names, very often it will be truncated. You do not need two first initials to indicate two first names. It will appear as follows:

Smithersonian, J, X

Example name: Johnathan, Xavier, Jacob Smith

If you have two last names, it is often times case dependent on length. It usually appears as two names, but if it is long enough it may remove the space and combine both names into one singular name. It will always match the license so if your license has the two names combined then the ID card should have both last names combined. In this example it is not long enough to be combined, so it will appear as:

Jacob Smtih, J, X

Example name: Jonathan, Xavier, Jacob-Smith

If you have a hyphenated last name, it will usually include the hyphen in the ID card. But once again to conserve space if the last name gets too long it may combine it as JacobSmith as if it was one word and one last name. In this example it is not long enough to be combined, so it will appear as.

Jacob-Smith, J, X

Example name: Jonathan, Xavier, Jacobson Smithersonian

As mentioned previously, if a last name is too long and two words, they most likely will combine both last names into one singular last name. The name would appear as follows:

JacobsonSmithersonian, J, X

Overall, this should give you an idea of how particular the NY DMV can be about how the name is formatted on the ID card. If it matches whatever it says on your license then you shouldn’t have anything to worry about. But remember if your name is longer than the average name you may have your name shortened or formatted in a certain way in order to fit on the insurance ID card.

There is one more factor that goes into the ID card, and it has to do with if you are transferring the license plate from one car to a new car. If you are transferring the registration from one car to another, the ID card will have the word “replacement” on it to indicate that it is replacing another vehicle on the policy and that the registration is being transferred. It is very important that you have the date that the registration is being transferred on it, along with it having the word replacement on it. This most often comes into play when you are trading in a car at a car dealership, but plates can be transferred on any vehicle for a multitude of reasons. Regardless of the reasoning, if you are keeping license plates from one car and putting it on a new car, the ID card must say REPLACEMENT.

Welcome to ny-insurance-info.com! This website is dedicated to people wanting to learn information about dealing with insurance in New York State. Often times, I have found that looking up information online about insurance can either be too broad, not state specific, or not accurate. This website is dedicated to giving out accurate information to New York residents about actual questions New Yorkers want to know about insurance.